Many investors assume that municipal bonds are always the best choice for high earners because of their tax-free income. But this common rule of thumb overlooks a key transition: retirement. High earners benefit from municipals during their peak earning years, but once they retire, their income—and tax bracket—often drops significantly. At that point, taxable bonds might provide higher after-tax income than municipals. How can you identify when this shift makes sense, and what steps should you take to optimize a fixed-income strategy?

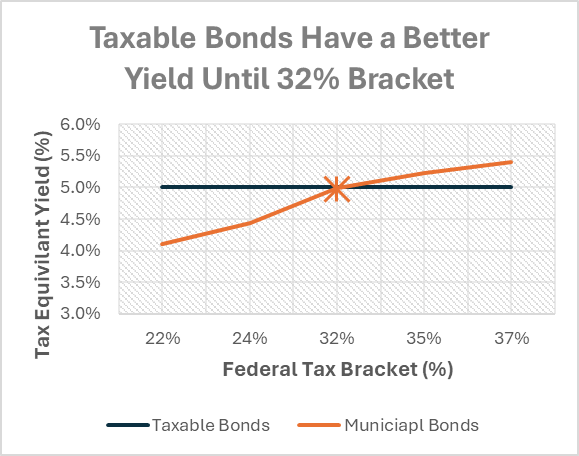

Identifying the opportunity (Fig. 1): With certain assumptions, municipal bonds look better only if you are in the 32% bracket or above. So, if you fall under that bracket at retirement and own municipal bonds, the opportunity may exist.

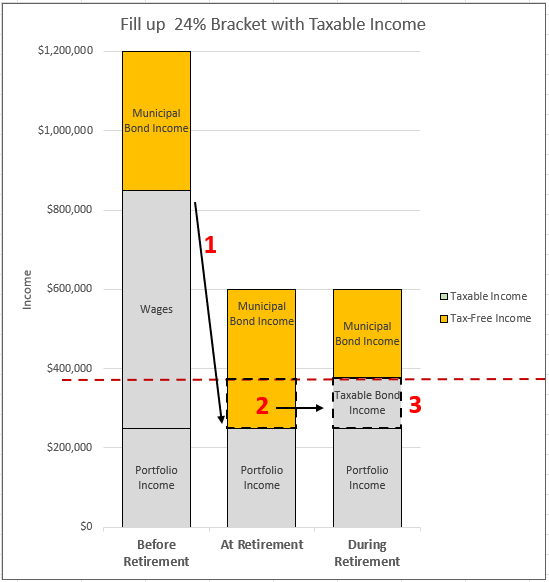

Steps to take (Fig. 2): Shift some tax-free income to taxable income to fill up the 24% bracket.

- Before Retirement – Income falls in the 37% tax bracket, but at retirement taxable income drops to under the 24% bracket (dashed red line).

- At Retirement – Identify how much income to swap from tax-free to taxable.

- During Retirement – After swapping, you now fill the 24% bracket, and created an optimal mix of bonds.

Visually:

This situation can be somewhat planned for in advance if retirement date and expected income is known. More commonly, year by year decisions can be made.

Summary: As tax brackets change in retirement, switching from municipal to taxable bonds can lead to more after-tax income. If your income drops below the 32% bracket, it may make sense to adjust your bond mix.

Assumptions: 5% taxable Bond; 3.2% Municipal. Credit quality or other characteristics not taken into account. 0% state income tax. NII tax included beginning 24% bracket.

Disclaimer

All calculations within are performed from scratch and, while diligent efforts are made to ensure accuracy, may contain unaudited errors. The content provided is for informational purposes only and should not be construed as investment advice, an offer, or a solicitation to buy or sell any financial instruments. Readers should consult with a qualified financial advisor for personalized advice tailored to their individual circumstances. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise, and cannot be applied directly to your situation. The information provided is based on general assumptions and may not apply to all individual situations. Tax laws, rates, and personal financial circumstances can vary, so it’s important to consult a financial advisor to tailor strategies to your specific needs.

Leave a comment