The 10-year annualized return on the US tech sector has been about 19.7%, vs. the total US market at 8.6%, US Small stocks at 7.7% and International at 4.9%. It seems pretty clear that tech has dominated, so why do most modern portfolios still include these other visibly underperforming assets classes? This article will hope to answer part of this question by briefly explaining modern portfolio construction.

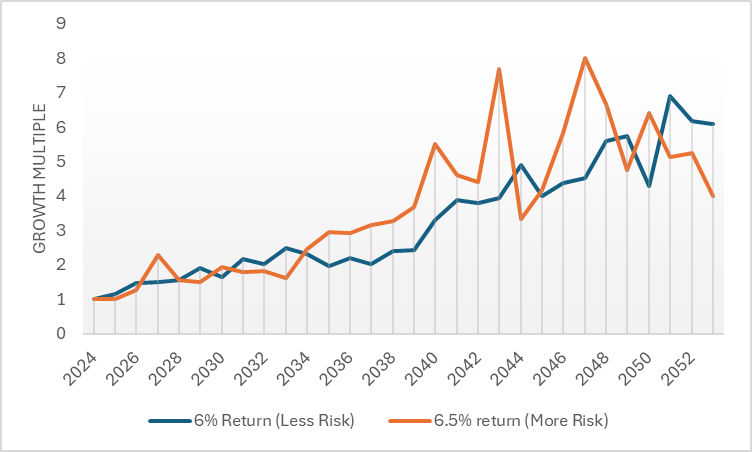

Starting from Scratch: The basis of modern portfolio construction is investing efficiently. In other words, the optimal portfolio is not the one that has the highest return, but rather the one that maximizes return per unit of risk. Given the choice between a safer portfolio earning 6% and a very risky portfolio earning 6.5%, most would choose the safer portfolio because taking extra risk to get an extra 0.5% exposes you to more downside as well.

The graph above visualizes taking on too much risk to get only marginally better returns. The orange portfolio may have a higher expected return, but the year-to-year experience is wildly different. Continuing with the initial example: US Tech is on the higher end for volatility… in recent years it has performed extremely well, but if you begin from March 2000 that number drops to 6.6% annual due to an initial period of very poor returns. More volatility = more chance for good and bad returns.

Back to the original question – why own multiple asset categories? The short answer is: Owning a combination of assets should result in a better return experience if the expected returns, expected volatility and correlations between them are modeled correctly.

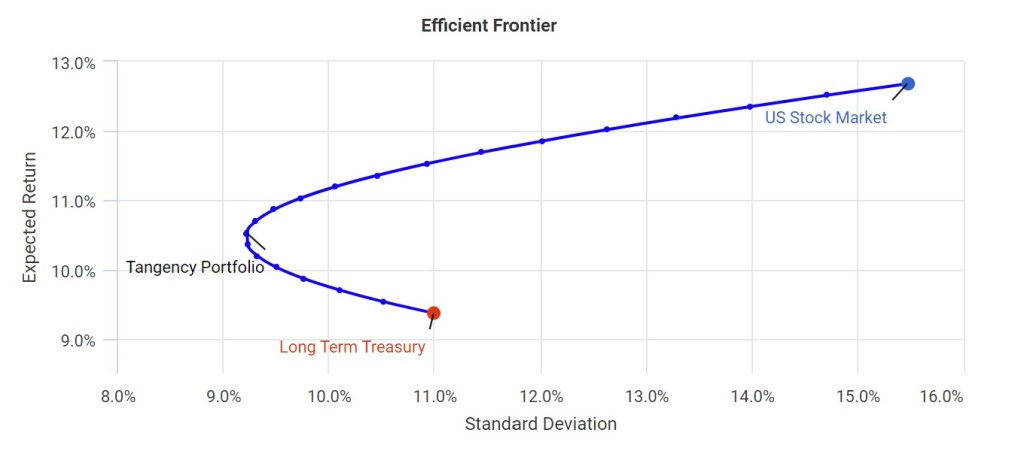

Below is a chart plotting what modern theory calls the Efficiency Frontier. It is too complex for purposes of this article, but the basic idea is relevant: For a given set of investments, there is a certain combination that provides the same expected return but with less volatility.

The theory would say why own only X or Y if owning them both will reduce volatility without compromising returns? Seems like a win-win. Is it still worth owning them both though, if one has a lower expected return? Experience would say yes: Investment grade bonds have a lower expected return than stock, yet many investors own them as a core part of their portfolio.

International stocks, small cap stocks, gold, real estate, all may have the potential to provide smoother returns. Just like any other asset however, they might not perform according to expectation. Expectations are primarily published by the securities analysis industry led by big banks, research firms and investment shops. For example, one of the largest investment banks published 2024 long-term assumptions giving Large Cap US stocks a lower expected return compared to International, Emerging, and “Value” stocks to name a few. Its anybody’s guess if that will turn out to be right.

Conclusions: Academics would say the reason to own different assets is to provide a smoother return experience. Sometimes this results in a lower expected return, but ideally much less volatility. The accuracy of these predictions relies heavily on assumptions for expected returns, expected volatility and expected correlations between assets.

Disclaimer

All calculations within are performed from scratch and, while diligent efforts are made to ensure accuracy, may contain unaudited errors. The content provided is for informational purposes only and should not be construed as investment advice, an offer, or a solicitation to buy or sell any financial instruments. Readers should consult with a qualified financial advisor for personalized advice tailored to their individual circumstances. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

Leave a comment