US Government bonds represent one of the largest and most heavily traded markets on the planet, and you’ve decided you need to own some. So which do you buy? This article will take a deep yet brief dive into the vastly different experiences an investor could have owning what look to be equal-return 5-year Treasury bonds.

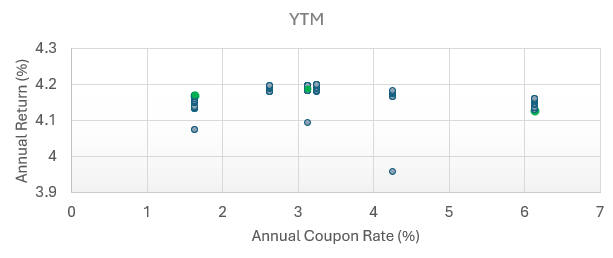

First, you’ll need to decide how they fit into your income plan, tax strategy etc. For now, lets just compare why that’s important: Below is a plot of the majority of Treasury Bonds maturing in August 2029, plotted by their coupon rate (interest income), and annual return. Here are three choices I’ve picked from the plot:

All things considered they all return about 4.15% annually over the next 5 years. So does it matter which one you buy? Maybe, it depends on if you need cash flow during the 5 year period.

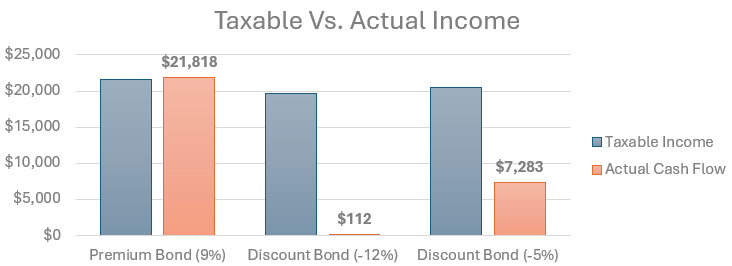

The bar chart below is a summary of reported vs. actual cash experience. In other words, considering all taxes, amortization etc…what actually gets deposited to your account? The blue bar is what gets reported on a tax return, the red bar is the total cash that gets put into your account over the 5 years, before the bond matures. Even though they have the same total returns, the discount bonds return the least cash to you before August 2029, and that might be a problem if you plan to live off bond income.

What drives this cash-flow difference? Ans: you pay tax on the discount bonds “accretion”, whereas you reduce your taxes on the premium bonds “amortization”. In other words: for the discounted bonds, most of the cash flow comes at maturity. You’ll likely be paying annual taxes on income you won’t see until year 5.

In conclusion, regardless of your income needs or purposes for owning bonds, it is important to know what your cash experience is going to be. Do your bonds pay you annual interest cash, or simply have maturities fund living expenses, or both? Design and implementation of your bond portfolio could be an extremely important factor in your financial success.

Calculation assumptions include:

• amortization of bond premium/discount

• tax rates (37% fed + 3.8% NII)

• prices on 7/22/2024

Disclaimer

All calculations within are performed from scratch and, while diligent efforts are made to ensure accuracy, may contain unaudited errors. The content provided is for informational purposes only and should not be construed as investment advice, an offer, or a solicitation to buy or sell any financial instruments. Readers should consult with a qualified financial advisor for personalized advice tailored to their individual circumstances. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

Leave a comment