Rebalancing – The practice of returning the values of certain assets in your portfolio to their prescribed percentages defined by an investment plan.

Marketed as an important piece of your investment plan, rebalancing is often misunderstood, or simply – practiced blindly. In other words, many do it automatically without first deciding if it makes sense. The root of this problem is that your portfolio is meant to be dynamic…meaning that over time, the percentage in bonds and stocks should change every so often to match your income & growth needs, risk, etc.

To illustrate the effect of lazy rebalancing, look at Figure 1. Here we have a portfolio set at 60% stocks and 40% bonds in year one. If you maintain that over the ten-year period, you can see that it reduces your return (orange). This is intuitive though…so why would you ever rebalance?

Here are two reasons why you would rebalance:

- If your stock portfolio fails to represent the overall market

This refers to buying or selling small amounts of one stock fund for another stock fund (not swapping stock for bonds). Trimming stock categories or buying more to keep them “in-line” assures you capture your benchmark stock return.

- If you mentally are not comfortable with the increased risk.

The blue line in Figure 1 begins with 60% stocks but ends with 81% stocks. During negative market returns, your portfolio will likely decrease more compared to the orange portfolio. Part of being a good investor means being able to sleep at night.

Here’s a reason you might not need to rebalance:

- If your income needs have not changed.

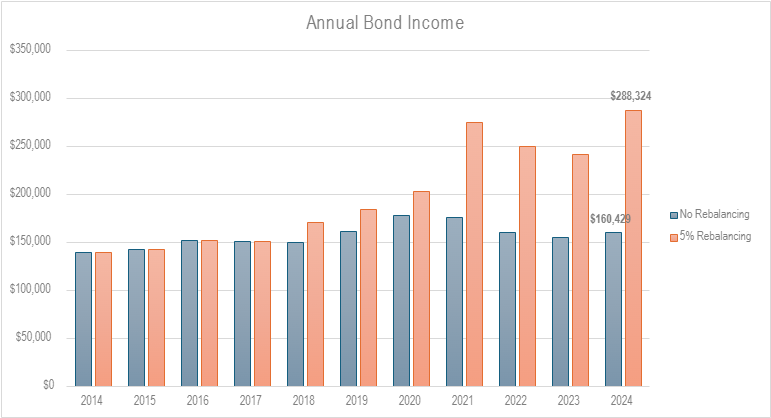

In Figure 1 both portfolios double in 10 years – a 40% bond allocation in year 10 would theoretically produce twice the amount of income than a 40% bond allocation in year 1 (see figure 2 below). Is that necessary? Maybe, maybe not, but you should have a reason. Without proper due diligence you could be unintentionally producing too much taxable income, reducing the growth potential of your portfolio.

In conclusion, rebalancing affects your portfolio returns. Over time that effect is probably negative, so it is very important to have good reasons for how your portfolio is constructed. At Belmont, we believe your mix of stocks v. bonds is one of the highest determinants of your portfolio return, and the reasoning behind it should be strong. Reach out to us if you’re interested in discussing if your current portfolio is in-line with what we’d recommend for you.

Disclaimer

All calculations within are performed from scratch and, while diligent efforts are made to ensure accuracy, may contain unaudited errors. The content provided is for informational purposes only and should not be construed as investment advice, an offer, or a solicitation to buy or sell any financial instruments. Readers should consult with a qualified financial advisor for personalized advice tailored to their individual circumstances. All investments are subject to a risk of loss. Diversification and strategic asset allocation do not assure profit or protect against loss in declining markets. These materials do not take into consideration your personal circumstances, financial or otherwise.

Leave a comment